Before 1987, I was on a path to one day having the largest shareholding in the company and being chairman — possibly chief executive. After 1987, that all changed.

I launched the AUS $2.25B takeover in August 1987 of John Fairfax Ltd., a large diversified media company that, at its height, included newspapers, television stations, radio stations, magazines, and newsprint mills. With The Sydney Morning Herald, The Age in Melbourne, and The Australian Financial Review, it had the equivalent of The New York Times, The Washington Post, and The Wall Street Journal of Australia.

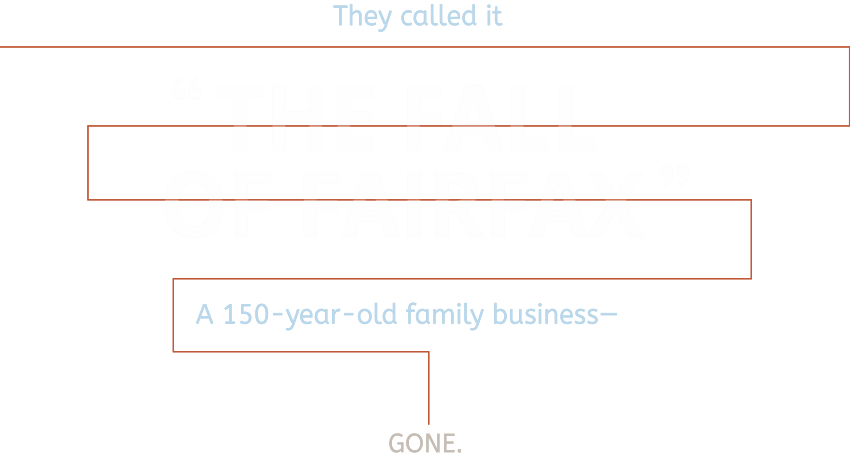

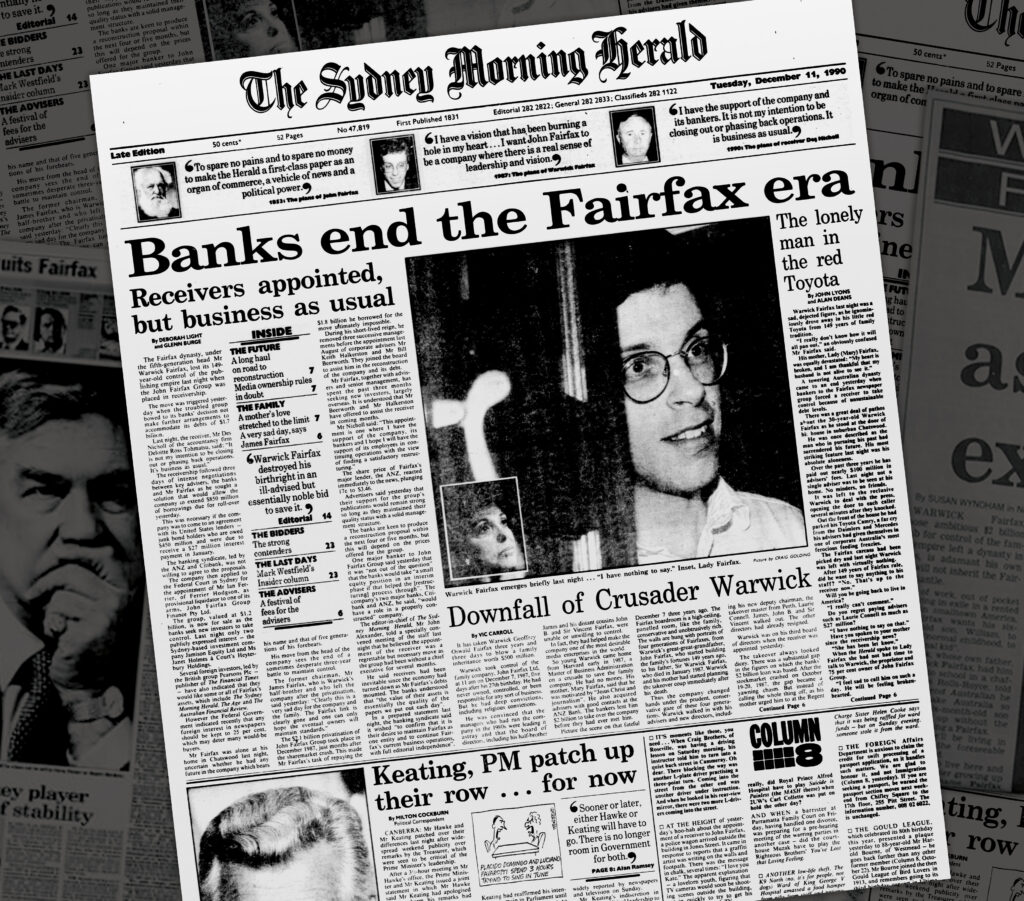

By December 1987, the company was over AUS $1.5 billion in debt. The debt was so large that when Australia went through a recession in 1990, the company went bankrupt — and the company passed out of family control.

It was the end of a dynasty.

The toughest experience of my life started in January 1987, when my father died.

Some family members had forced my father to resign as Chairman in 1976. He remained on the board until his death, but he had issues with how the company was being run. My father was a man I greatly admired and revered; after his death, I felt his mantle had fallen to me. I was 26 and in my last year at Harvard Business School.

In early 1987, there was a rise in the company’s stock price. The market seemed to feel that the company was “in play” following my father’s death. I felt that the company was not being managed well — and not according to the ideals of its founder, my great-great grandfather, John Fairfax.

Corporate raiders were lurking. I felt that I had no choice but to try everything in my power to preserve family control of the company and to ensure that it was well run in line with the ideals of John Fairfax.

While my classmates were studying for final exams in our last semester at Harvard,

I was on the phone with business associates in

Australia discussing a takeover bid.

In August 1987, I launched an AUS $2.25B takeover bid for John Fairfax, Ltd. It was considered one of the largest takeovers in Australian corporate history at the time.

Almost from the beginning, things went wrong. Other major family shareholders sold out. The October 1987 stock market crash hurt our asset sale program, lowering the prices we expected to receive. It all led to a crippling debt load.

I brought in a new chief executive, who succeeded in increasing operating profits by 80% in his first year. We tried numerous refinancings to stabilize the effect of the significant debt load. But by 1990, Australia was hit by a recession, which had a major effect on profitability.

With the amount of debt we had, there was no margin for error.

The result: in late 1990, the company was forced to

file for bankruptcy.

The decade after the company went into bankruptcy was crippling for me.

I had made many mistakes and poor assumptions. When the company’s stock price rose early in 1987, was the company really in danger — especially if the large family shareholders stuck together? Why would they want to remain in a privatized family company that I controlled? While my father and I may have had issues with how the company was being run, was the takeover really necessary?

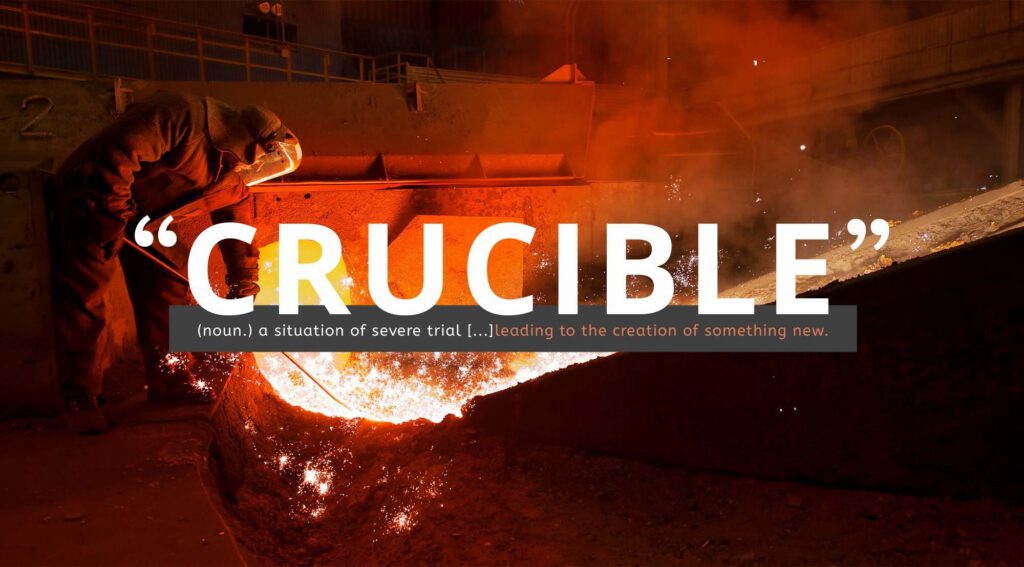

Though this was very painful,

OUT OF A DEVASTATING CRUCIBLE CAME A GREAT BLESSING.

And born out of all of this came a philosophical approach to living and leading a life of authenticity and significance.

Subscribe to the  today.

today.